Signal > Noise – The Rot is Coming Home to Roost in the US

February 18, 2026

Noise

Unfortunately, the geopolitical situation around the world, and in the United States in particular, isn’t getting better.

Unfortunately, the “around the world” part has gotten a lot closer to home in the past year. No longer are we watching proxy wars and genocide in the distant Middle East, but we are seeing NATO needing to rally against a Trump government threat to take over Greenland, and hearing that the Canadian Military is actually forming contingency plans regarding a ground invasion from the United States.

Unfortunately, this past Saturday I woke up and had the misfortune of checking the news and seeing masked United States federal agents execute an unarmed man in the street. This was the second execution of an US citizen by their own government within a month. The situation in Minnesota continues to escalate despite calls from all levels of government for the Department of Homeland Security and ICE to de-escalate.

The most difficult part of the work I do for you is separating: “What terrible things are happening at home and around the world?”, from: “What will affect investments, and how?”. This can be particularly unpleasant when world events get into an ugly streak, and yet many of those distasteful events do not require taking action in portfolios.

Signal

Determining true Signal at a time like this is a frustrating practice. Taking note of the “Noise” driving headlines and then stripping away the narrative to see what truly matters and where the effects are being felt is what I created this newsletter for. Relying on factual information, such as official economic releases, commercial reporting, and market statistics will always form the core of determining prudent financial positioning.

So, let’s try to get beyond the headlines and take a closer look at the international markets and their adjustments to the Trump regime in America by focusing on one particularly noisy issue right now: Threats against Greenland sovereignty.

The Greenland Noise – Trump threatens to take over Greenland by force and muses about making Canada a protectorate. NATO points out that this is in direct violation of the treaty. Member nations rally behind Denmark and Greenland. In the midst of this, PM Mark Carney takes the stage at Davos and urges increased coordination between “middle powers” in order to keep increasingly unstable partnerships (and leadership) of the superpower nations in check. Trump sends a letter to Norway saying the reason he is comfortable using force is because he was not given the Nobel Peace Prize, which of course is not issued by Norway, and has nothing to do with Greenland. NATO country leaders leave Davos prior to Trump arriving to speak.

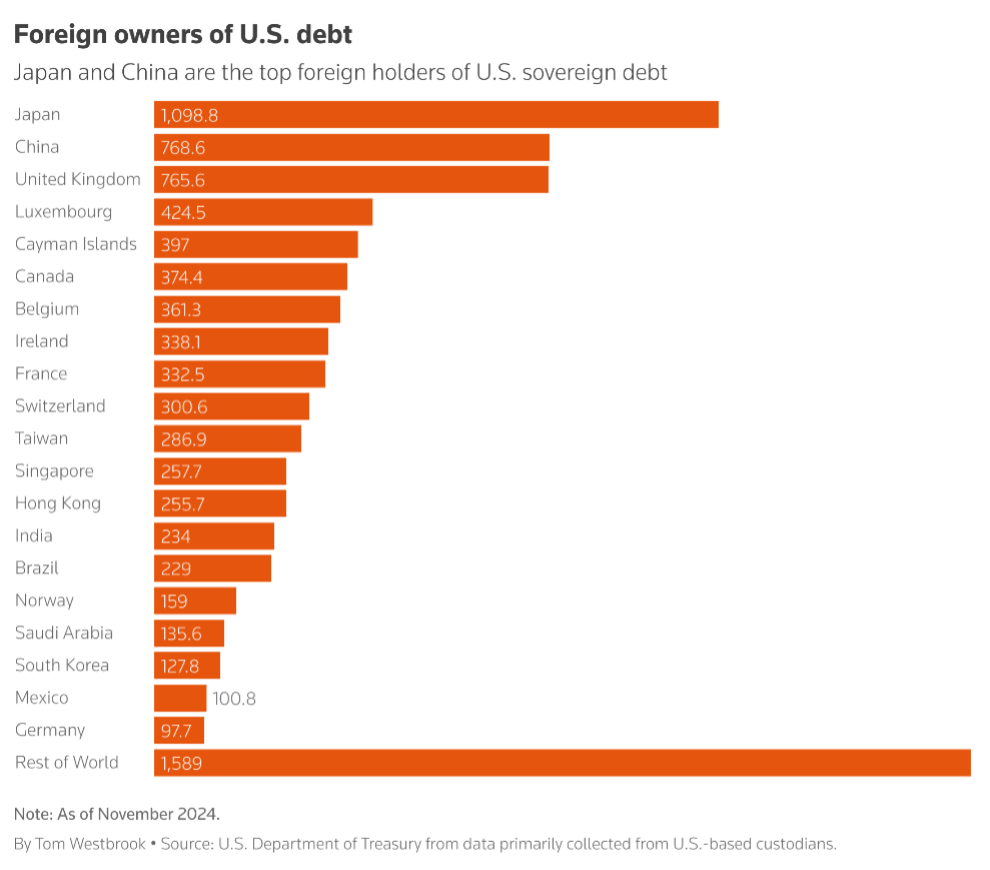

The Greenland Signal – As the US threat against a NATO member nation hit the headlines, the most important thing to happen to your finances was not the threat of war, it was the action subsequently taken by Danish and Swedish pension funds who continued increasing their sales of US Treasuries. Not exactly a ripper of a headline there. However, in terms of overall impact, this rejection of US Treasures at the sovereign level is a significant and serious issue for the United States and the US Dollar as the international reserve currency of choice since the end of WWII.

What Happens Next - Taken down the road a few steps, the sale, or even simply ceasing to repurchase maturities, of US Treasuries by foreign nations means that the US now has issues paying its current bills. A great deal of US (and other sovereign) financing is achieved by “rolling” their debt forward – issuing new bills in order to pay off the old ones. When the borrower (the US) is trustworthy and creditworthy, this is fairly standard procedure. However, if the US is unable to roll forward those bonds, new dollars need to be issued so that the US can buy back its own debt (increasing inflation / devaluing the USD), and credit rating agencies lower their “trustworthiness” opinions (making US debt more expensive).

Given that US Treasury issuance in 2025 faced more undersubscription (not enough buyers for the debt the US needed to sell) then in previous years, and at the same time the US needs to increase overall issuance due to regular maturities (not even including the heaps of new US debt being issued under Trump), the threat of additional sales from foreign nations is a massive issue as no one will want to be the last person holding if and when the dam breaks.

(source)

(source)

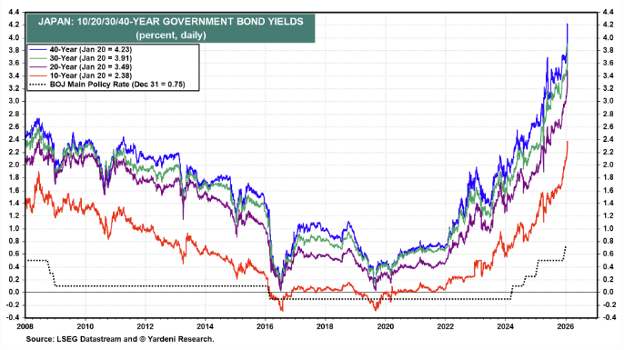

“The sovereign bond market is too big; this can’t happen in the real world.” Wondering what a sovereign debt unwind looks like in real time? Take a look at lending rates in Japan right now. Historically among the lowest rates in the world, bond traders have flipped opinions on whether the BOJ and Japanese government will be able to continue holding rates artificially low for much longer. The spiking yield in the chart below indicates the plummeting value of long bonds, which then leads to more investors rushing to the exits. This is a crippling loss of long-term value for Japanese bond investors.

(source)

(source)

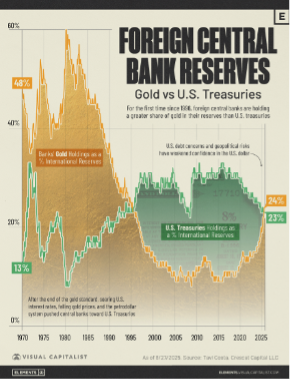

Even more troubling for the USD, as the international reserve currency of choice and historically as a mandatory business transactional currency due to the dominance of US banking overseas, after a historic jump in valuation during 2025, Gold has just retaken the top spot in international reserve valuations.

(source)

(source)

The headlines about bond valuations, foreign ownership levels, and the fragile stability of international reserves will rarely make the front page, but these are all extremely useful for ensuring portfolios are protected from predictable vulnerabilities.

Takeaways:

US government bonds are starting to be priced more precariously than their credit ratings would indicate (credit ratings are never leading indicators);

US dollar-denominated assets may fall in value if their finances deteriorate (rapid currency changes can affect total return as much or more than investment performance);

For all their bluster militarily, the US’s strength in global finance is also proving to be a weakness (current dominance has previously been backed by reliability and stability, which is now failing).